Entering U.S. Markets? Your Disclosure Strategy Needs to Change

- Melissa Strle

- Apr 23

- 5 min read

Disclosure Intelligence Series How disclosure works in modern capital markets

Most companies treat a U.S. stock exchange listing as a structural milestone. In practice, it represents something more significant. Entering U.S. markets is not just a listing event. It is a fundamental shift in how a company’s information is communicated, interpreted, and acted on.

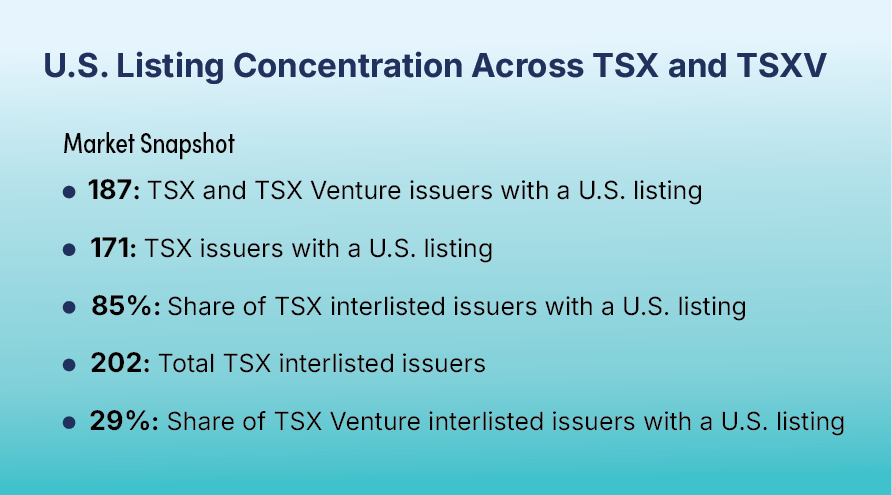

As of March 2026, 187 TSX and TSX Venture issuers are interlisted on U.S. exchanges, within a broader group of 258 interlisted companies globally.

This shift into U.S. market participation is not evenly distributed. It is concentrated among more senior issuers.

85% of TSX interlisted issuers maintain a U.S. listing, compared to just 29% of TSX Venture issuers.

As companies scale into these markets, they are not just moving exchanges. They are entering a fundamentally different disclosure environment.

This is where disclosure strategy needs to change.

The Shift Most Companies Underestimate

Cross-border listings are a cornerstone of the Canadian market, particularly among dual-listed companies operating in both Canada and the U.S.

The density of these listings changes significantly as companies scale. U.S. listings are far more common among TSX issuers than among TSX Venture companies.

The motivation is clear. Companies are seeking greater visibility, deeper liquidity, and access to a broader investor base.

What is less often considered is how different the communication environment becomes.

Canada has approximately 3,700 listed companies across the TSX and TSX Venture Exchange. Nasdaq alone hosts over 4,000 companies, including 4,075 listed on The Nasdaq Stock Market as of December 31, 2024.

At the same time, exchanges such as the NYSE bring together hundreds of international issuers from dozens of countries, all competing for investor attention.

With more issuers competing for the same investor attention in the U.S., the pace and expectations of communication shift.

In this context, communication becomes more continuous, more competitive, and more dependent on visibility.

As a result, disclosure becomes increasingly complex to manage.

By the Numbers: Interlisted Activity in March 2026

The numbers show how U.S. listings are distributed across TSX and TSX Venture issuers.

Note: TMX Group data as at March 2026.

The concentration of U.S. listings increases as companies move up to the TSX.

At the same time, entry into U.S. markets brings higher disclosure expectations and more intense competition for attention.

Why Disclosure Strategy Needs to Adapt

When Canadian companies enter U.S. markets, the underlying principles of disclosure do not fundamentally change, but the environment in which they operate does.

Requirements around timely and broad disclosure of material information remain consistent across jurisdictions, supported by frameworks such as Regulation FD in the U.S. and National Policy 51-201 in Canada. In Canada, material changes must be disclosed through a news release, followed by a regulatory filing. In the U.S., companies must ensure broad public dissemination, but no single method is mandated. In practice, disclosure is achieved through a combination of filings, news releases, and other public channels.

U.S. markets have a higher concentration of issuers and greater analyst coverage, resulting in a more continuous flow of information. In this environment, material information is expected to reach the market quickly, with greater emphasis on how effectively it is interpreted.

In this environment, visibility does not naturally follow from a U.S. listing. It depends on how effectively material information competes for attention and reaches the market. These differences do not change what must be disclosed, but they require disclosure strategy to adapt.

As a result, disclosure begins to function not just as a compliance requirement, but as part of a company’s communication infrastructure.

"In today’s markets, disclosure is not just compliance. It is infrastructure."

Visibility is No Longer Just About Reach

It is easy to think of press release distribution in terms of reach, or how widely information is disseminated. But reach alone does not determine whether information is actually seen, understood, or acted on.

Investor awareness now develops across multiple layers, including brokerage platforms, institutional workflows, financial data systems, and aggregation tools. Information does not move through a single channel. It moves through a network of systems that filter, surface, and prioritize what investors ultimately see.

Even when widely distributed, disclosures can be overlooked. Visibility depends not just on reach, but on where information appears, when it reaches the market, and how consistently and clearly it is presented across the channels investors use.

This makes the structure and timing of disclosure just as important as distribution itself.

Disclosure Challenges for Dual-Listed Companies

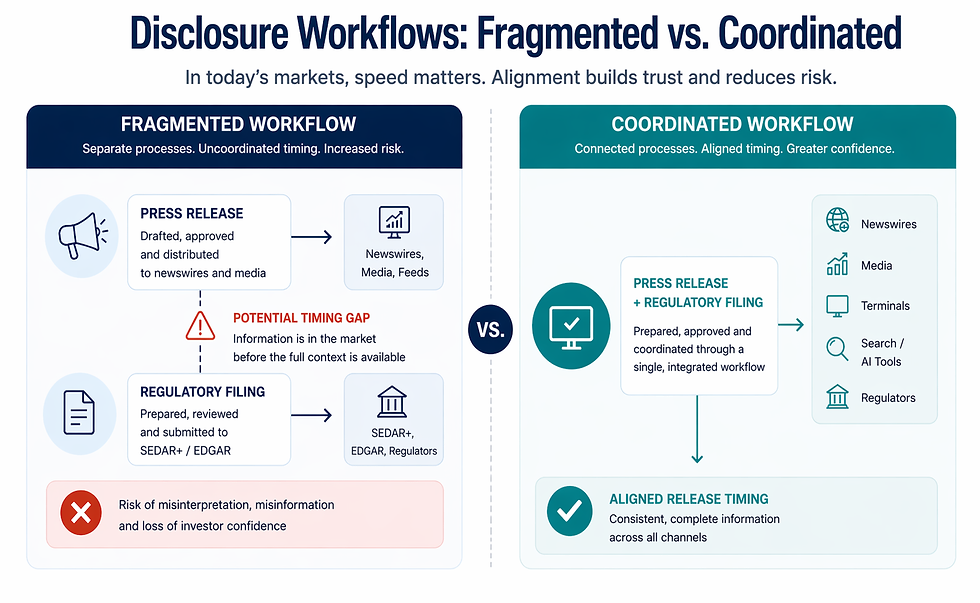

One of the most important, and least visible, challenges for dual-listed companies is coordination.

In practice, disclosure is not a single action. It typically involves preparing a press release alongside regulatory filings, coordinating internal approvals, and aligning timing across multiple systems.

In many organizations, these steps are handled across separate teams, tools, and vendors rather than through a single integrated workflow.

This creates a timing gap. Between the moment a press release is issued and the corresponding filing is made, there is often a window where information is already being interpreted, shared, and acted on, sometimes before the full context is available.

These gaps are rarely intentional. They are typically the result of siloed processes or technical bottlenecks, such as XBRL preparation requirements or payment-related delays, which can disrupt even well-planned disclosure timelines.

Over time, this fragmentation introduces coordination challenges that often only become apparent when companies are operating under tight timelines.

For dual-listed companies operating in sectors such as mining and life sciences, this risk can be more pronounced. In these industries, key announcements are often outcome-driven, where results can be interpreted quickly as either positive or negative.

In modern markets, investors access information through a wide range of sources, including news feeds, brokerage platforms, exchange-integrated systems, and company disclosures.

What This Means in Practice: Disclosure Intelligence

In U.S. markets, these dynamics are not theoretical. They directly change how disclosure needs to be executed.

Fragmented workflows create risks that can become more visible and more difficult to manage.

Leading issuers are adopting a more structured approach to disclosure. This approach can be understood as Disclosure Intelligence.

Companies can improve disclosure execution by adopting a more coordinated and structured approach, as reflected in the following principles:

Integrated Align press releases and regulatory filings as closely as possible in both timing and content. In fast-moving markets, even small gaps can lead to incomplete information being interpreted and acted on before full context is available.

Consistent Treat communication as continuous rather than event-driven. Instead of relying solely on major announcements, maintain a steady flow of clear, consistent updates to remain visible within the systems investors actually use.

Structured

Prepare information in a consistent and structured format. This improves clarity for investors and ensures disclosures can be reliably interpreted by the data systems, platforms, and AI models that increasingly shape how information is surfaced.

Intentional

Reassess distribution and workflow decisions following a market transition. Recognize that legacy approaches often reflect a different environment and may not align with how investors access and evaluate information in U.S. markets.

Simplified

Reduce fragmentation across teams, tools, and processes to improve both speed and clarity. In coordinated market environments, complexity becomes a liability.

Together, these principles set the standard for how disclosure is executed in modern markets.

A Broader Shift

Expanding into U.S. markets is often framed in terms of scale. More investors, more visibility, more opportunity.

But it also requires a different approach to communication. This approach reflects how information is distributed, consumed, and acted on in modern markets.

Companies that recognize this early are better positioned to maintain clarity, consistency, and trust as they grow.

Because in today’s markets, disclosure is not just compliance. It is infrastructure.

The Disclosure Strategy Health Check

Ask your team these three questions to determine if your current strategy has kept pace with your market transition:

Is your news distribution reaching investors through the platforms they actively use to access and act on issuer information?

Are your press releases and regulatory filings managed through a single, coordinated workflow?

Has your communication strategy evolved since your last listing event, or are you still following a legacy “default”?